Creating a legally sound and comprehensive promissory note is crucial for establishing financial agreements and ensuring accountability. Whether you’re a business owner seeking to secure funding, an individual establishing a loan, or a freelancer offering services, a well-drafted promissory note provides clarity and protects all parties involved. This guide provides a detailed overview of what to include in a California-compliant promissory note, covering essential clauses and best practices. Understanding the nuances of California law is paramount when creating and utilizing these documents. This template offers a solid foundation, but it’s always recommended to consult with an attorney to ensure it meets your specific needs and complies with all applicable regulations.

Why a Promissory Note is Essential

A promissory note is a legally binding agreement where one party (the borrower) promises to pay another party (the lender) a specific sum of money (the principal) on demand or at a future date. It’s a fundamental tool for managing financial relationships and mitigating risk. Without a clear and enforceable promissory note, disputes can arise, leading to costly legal battles. A well-structured note provides a documented record of the agreement, protecting both parties and facilitating smooth transactions. It’s particularly vital for business loans, personal loans, and agreements between individuals. The California legal system emphasizes the importance of clear and unambiguous contracts, and a promissory note is a cornerstone of that framework. Furthermore, it’s increasingly common for businesses to use these notes to secure lines of credit, demonstrating a commitment to repayment.

Understanding the Core Components of a California Promissory Note

Before diving into the specific clauses, it’s important to grasp the fundamental elements required by California law. A California promissory note must adhere to the following principles:

- Clear Identification: The note must clearly identify all parties involved – the borrower and the lender.

- Principal Amount: The amount of money being borrowed must be specified precisely.

- Interest Rate (if applicable): If interest is being charged, the rate must be clearly stated.

- Payment Schedule: A detailed schedule outlining when and how the principal and interest will be repaid.

- Default Provisions: Clearly define what constitutes a default and the consequences of failing to meet obligations.

- Legal Compliance: The note must comply with all applicable California statutes and regulations.

Key Clauses and Considerations in a California Promissory Note

Let’s examine some of the most important clauses to include in your California promissory note:

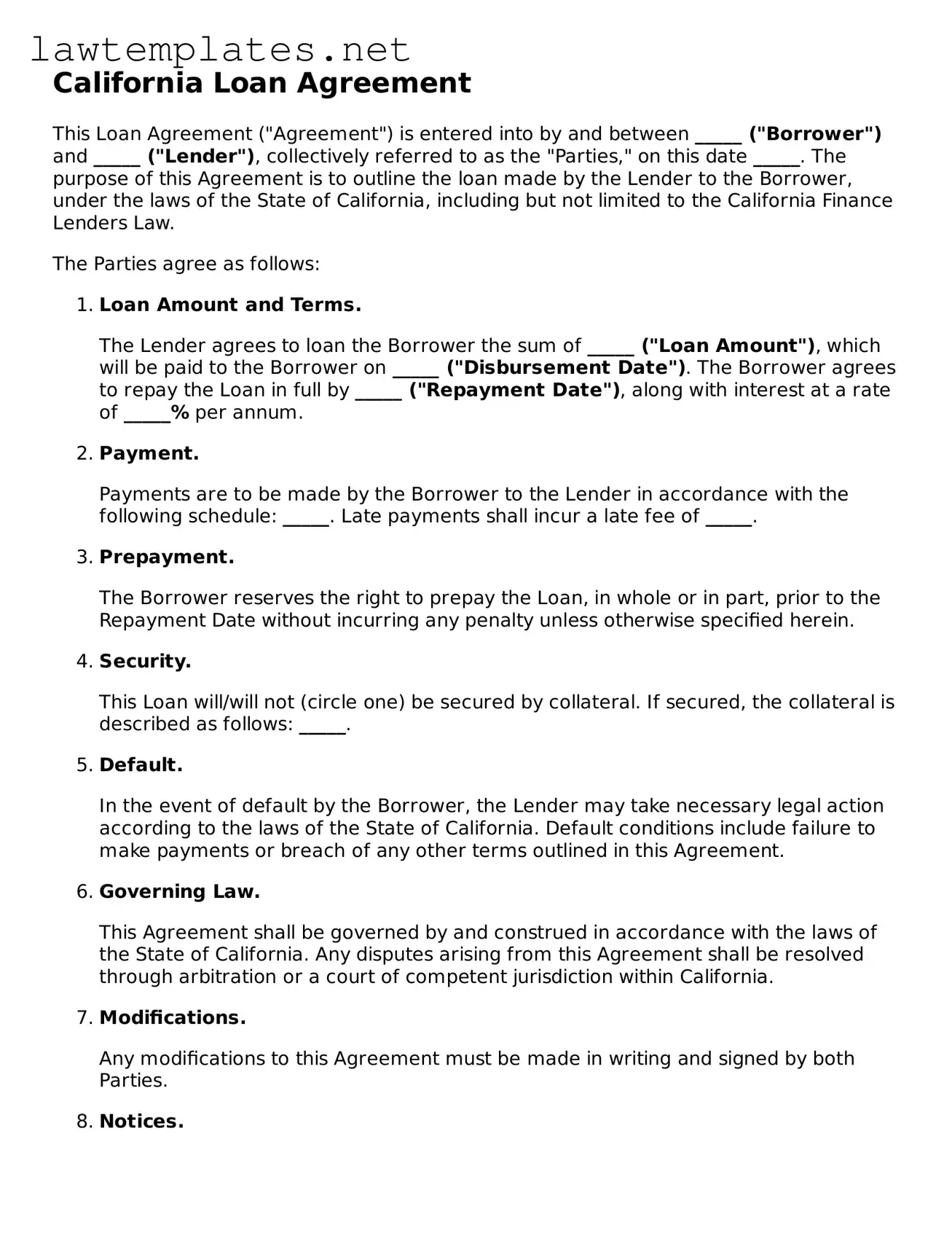

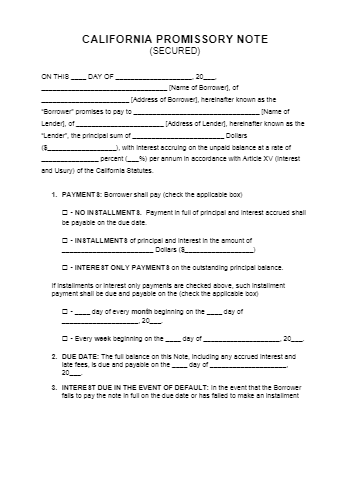

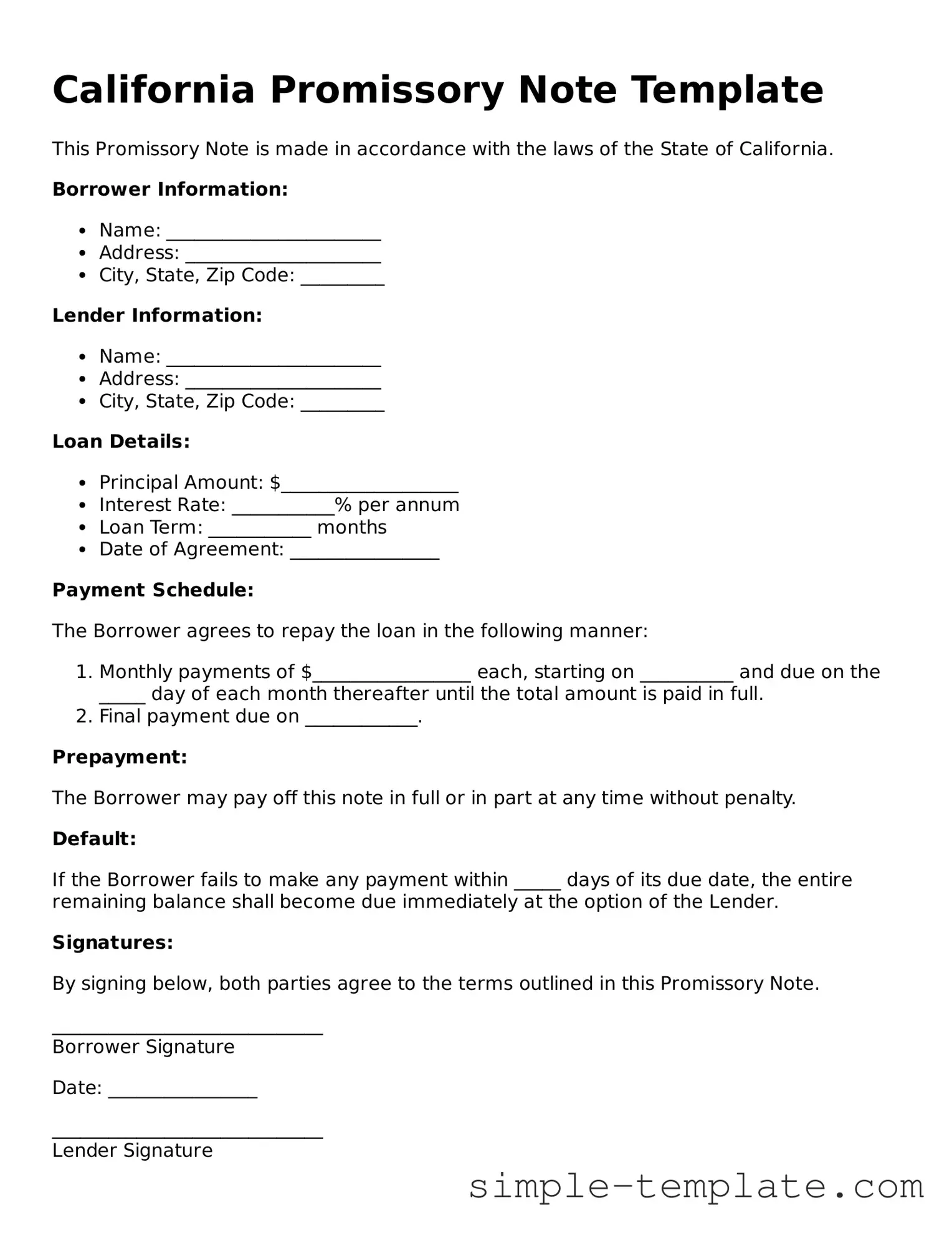

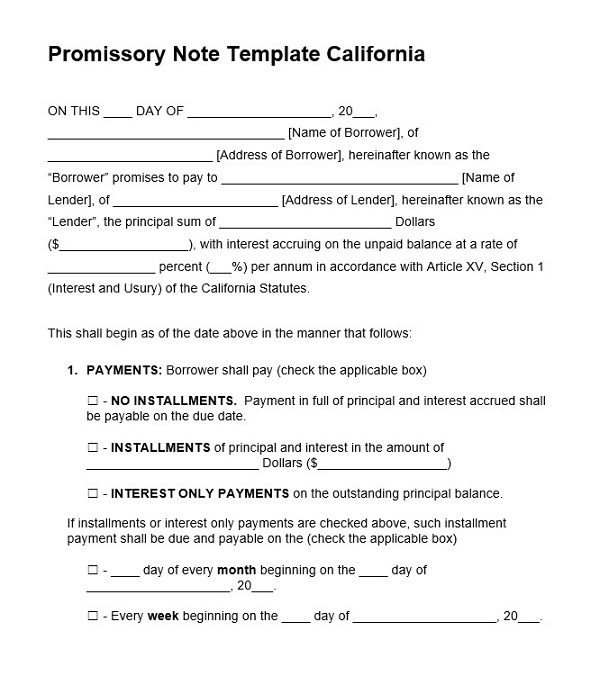

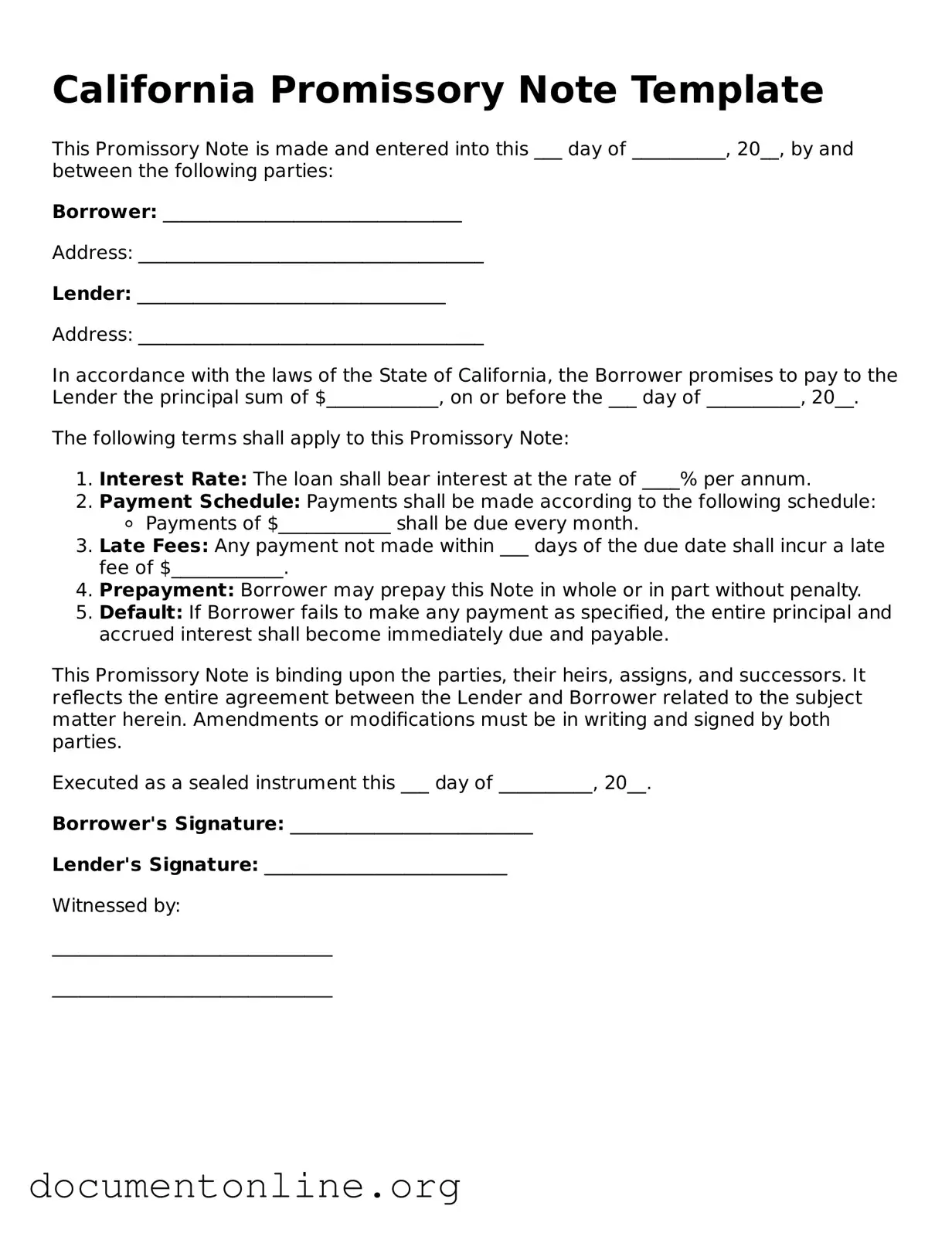

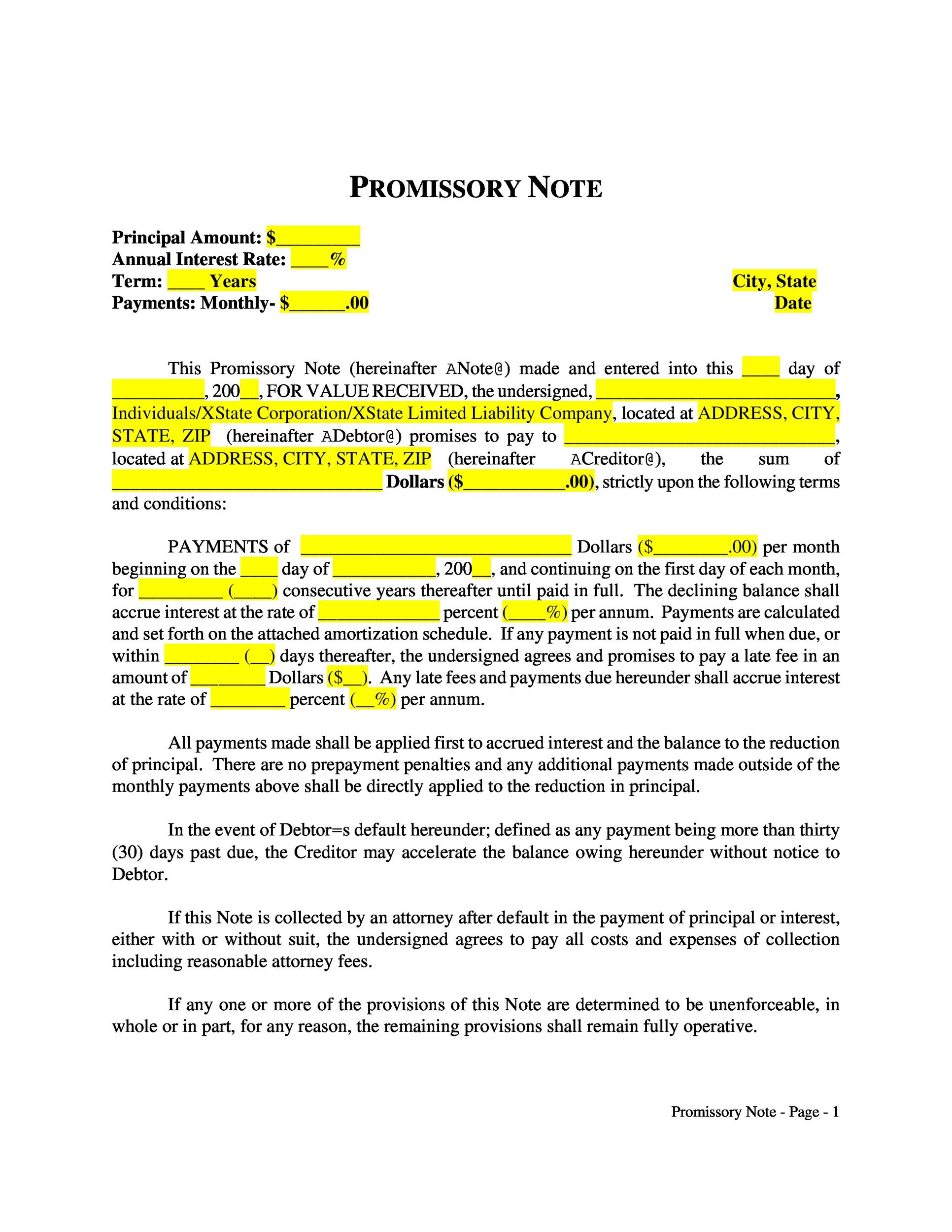

1. Parties Involved

The first section of the note should clearly identify the borrower and the lender. This includes full legal names, addresses, and, if applicable, the legal entity (e.g., corporation, LLC) they represent. It’s crucial to accurately reflect the parties’ identities to avoid future disputes. For example, “John Doe, residing at 123 Main Street, Anytown, CA, hereinafter referred to as ‘Borrower’ and Jane Smith, residing at 456 Oak Avenue, Anytown, CA, hereinafter referred to as ‘Lender’.”

2. Principal Amount and Interest

The note must explicitly state the total amount of the loan and the interest rate (if any). It’s advisable to specify the currency used (e.g., USD, EUR). For example: “The principal amount of this promissory note is $10,000.00 (Ten Thousand Dollars), and the interest rate shall be charged as follows: 5% per annum, payable monthly.”

3. Payment Schedule

This section details how and when the principal and interest will be repaid. It’s vital to provide a realistic and detailed schedule. Consider including:

- Payment Frequency: Monthly, quarterly, annually, etc.

- Payment Due Dates: Clearly specify the date each payment is due.

- Payment Method: Specify how payments will be made (e.g., check, wire transfer).

- Late Payment Penalties: Outline the consequences of late payments (e.g., late fees, suspension of interest).

4. Default and Remedies

This section outlines what constitutes a default and the remedies available to the lender. It’s essential to define the consequences of failing to meet obligations, such as:

- Acceleration of Debt: The lender has the right to demand immediate repayment of the entire principal amount.

- Legal Action: The lender can initiate legal action to recover the debt.

- Collection Efforts: The lender can pursue collection efforts, including lawsuits and wage garnishment.

5. Collateral (if applicable)

If the loan is secured by collateral (e.g., equipment, real estate), the note must clearly identify the collateral and specify the terms of the security agreement. This is a critical element for protecting the lender’s investment. For example: “The loan is secured by the equipment located at 789 Pine Lane, Anytown, CA. The lender shall have a security interest in the equipment.”

6. Governing Law and Dispute Resolution

Specify the state law that will govern the interpretation and enforcement of the note. Consider including a clause specifying the method for resolving disputes, such as mediation or arbitration. This helps to streamline the process and reduce the likelihood of costly litigation. For example: “This promissory note shall be governed by and construed in accordance with the laws of the State of California.”

California Law and Promissory Notes

California law places significant emphasis on the enforceability of promissory notes. The California Supreme Court has consistently ruled that a promissory note must be clear, unambiguous, and reasonably supported by consideration. Any ambiguity or vagueness in the note can be challenged in court. Furthermore, the note must accurately reflect the parties’ intentions and avoid misleading statements. It’s always advisable to seek legal advice to ensure your promissory note complies with all applicable California laws and regulations.

Conclusion

Creating a robust and legally sound promissory note is a critical step in establishing a successful financial relationship. By carefully considering the key components outlined in this guide, and consulting with an attorney, you can ensure that your note is comprehensive, enforceable, and protects your interests. Remember that the specific requirements of a promissory note may vary depending on the nature of the transaction and the applicable state law. Proper planning and attention to detail are essential for minimizing risk and maximizing the likelihood of a successful outcome. Investing in legal counsel is a worthwhile investment to safeguard your financial future.

Conclusion

Ultimately, a well-drafted promissory note serves as a vital tool for managing financial obligations and fostering trust between borrowers and lenders. By adhering to California law and incorporating the essential clauses outlined in this guide, you can create a document that provides clarity, protects your interests, and promotes a stable and reliable financial relationship. Regular review and updates to the note as circumstances change are also crucial for maintaining its effectiveness.