The world of business can be complex, and securing funding is often a critical step towards growth. One of the most common and vital financial instruments for businesses is the Revolving Credit Facility Agreement. This agreement allows businesses to borrow funds up to a pre-defined limit, providing flexibility and operational support. Understanding the nuances of these agreements is paramount for both lenders and borrowers. This article will delve into the key components of a Revolving Credit Facility Agreement Template, providing a comprehensive overview for businesses considering this crucial financial arrangement. Revolving Credit Facility Agreement Template – a cornerstone of modern business finance.

Understanding the Basics of a Revolving Credit Facility

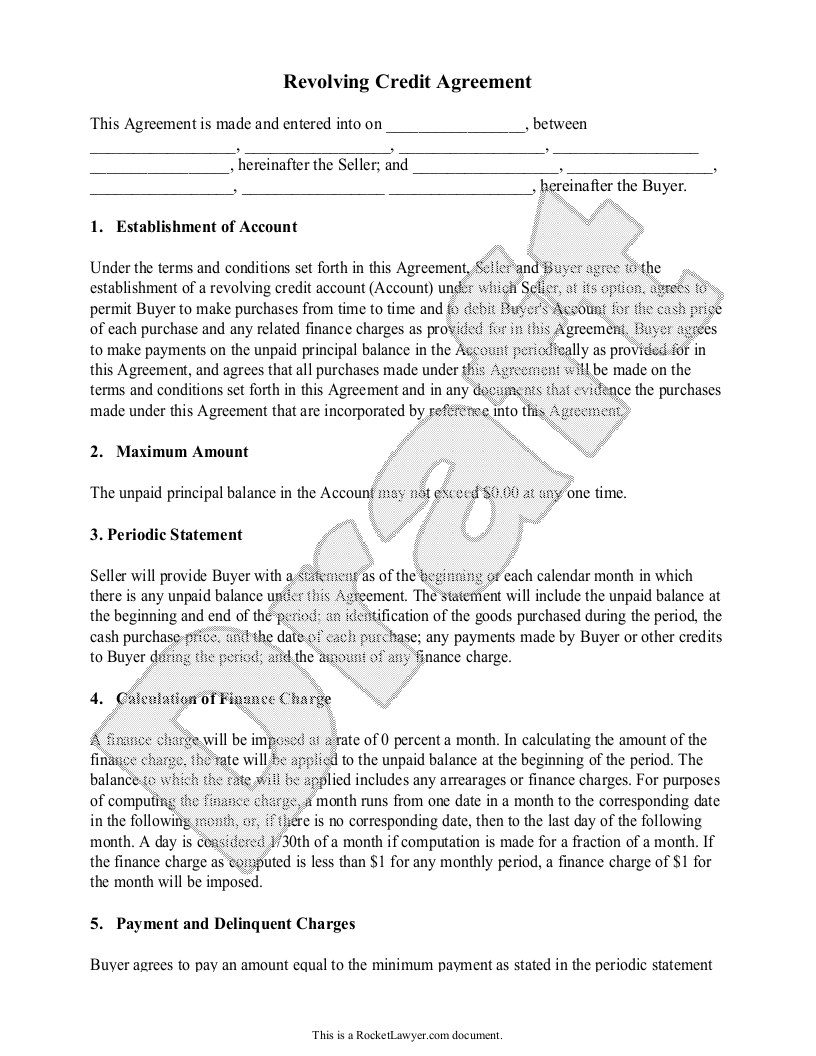

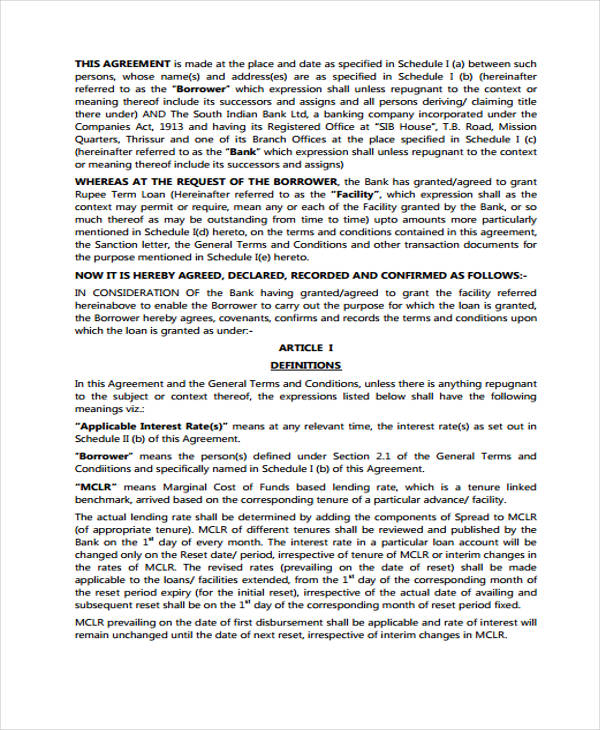

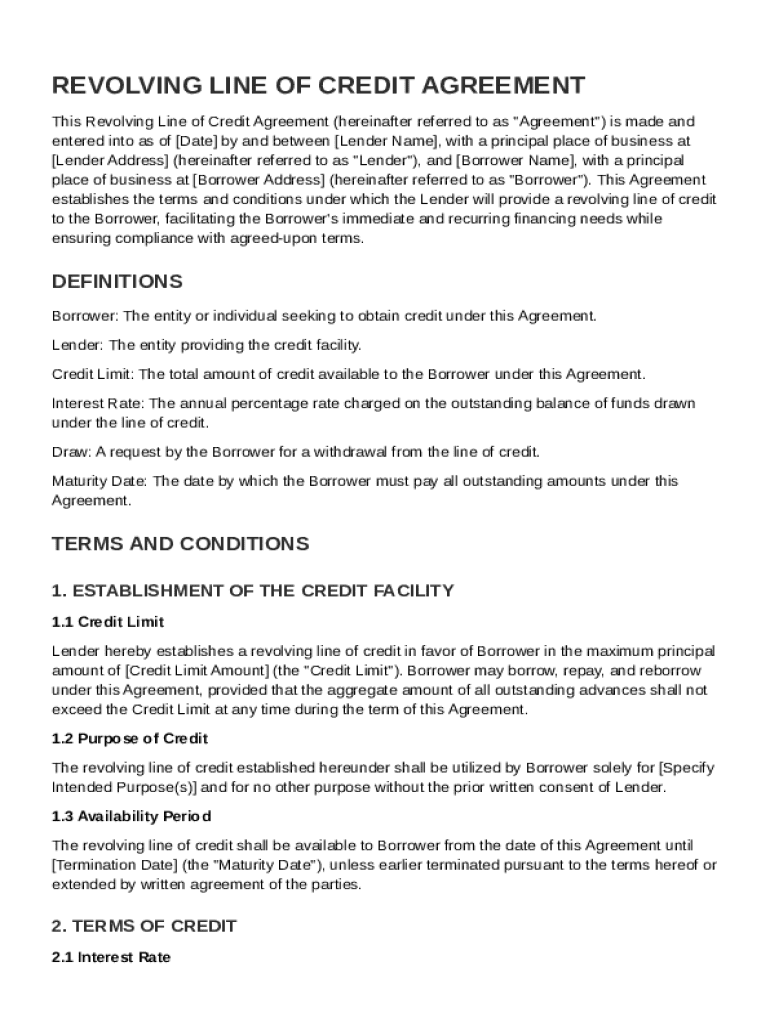

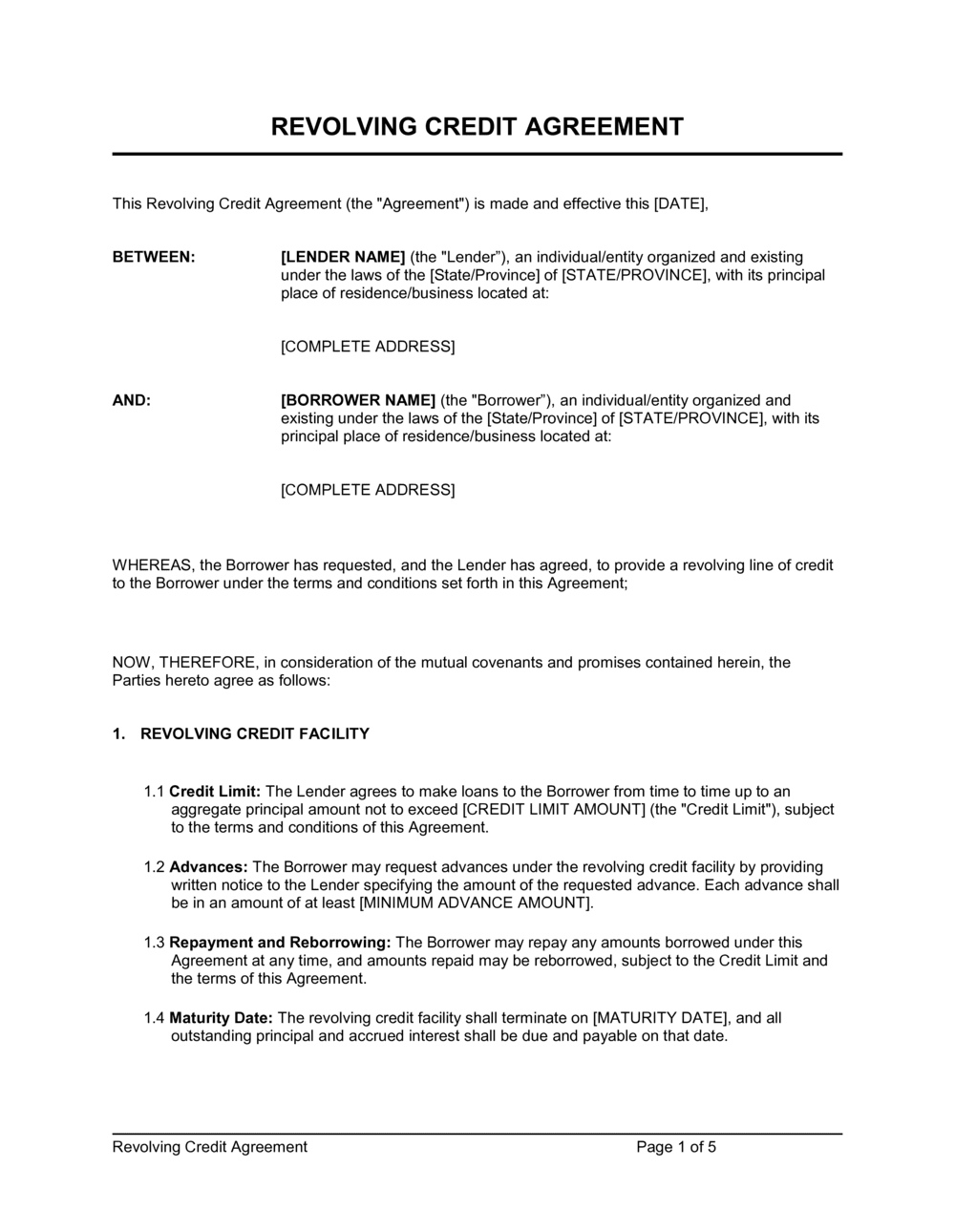

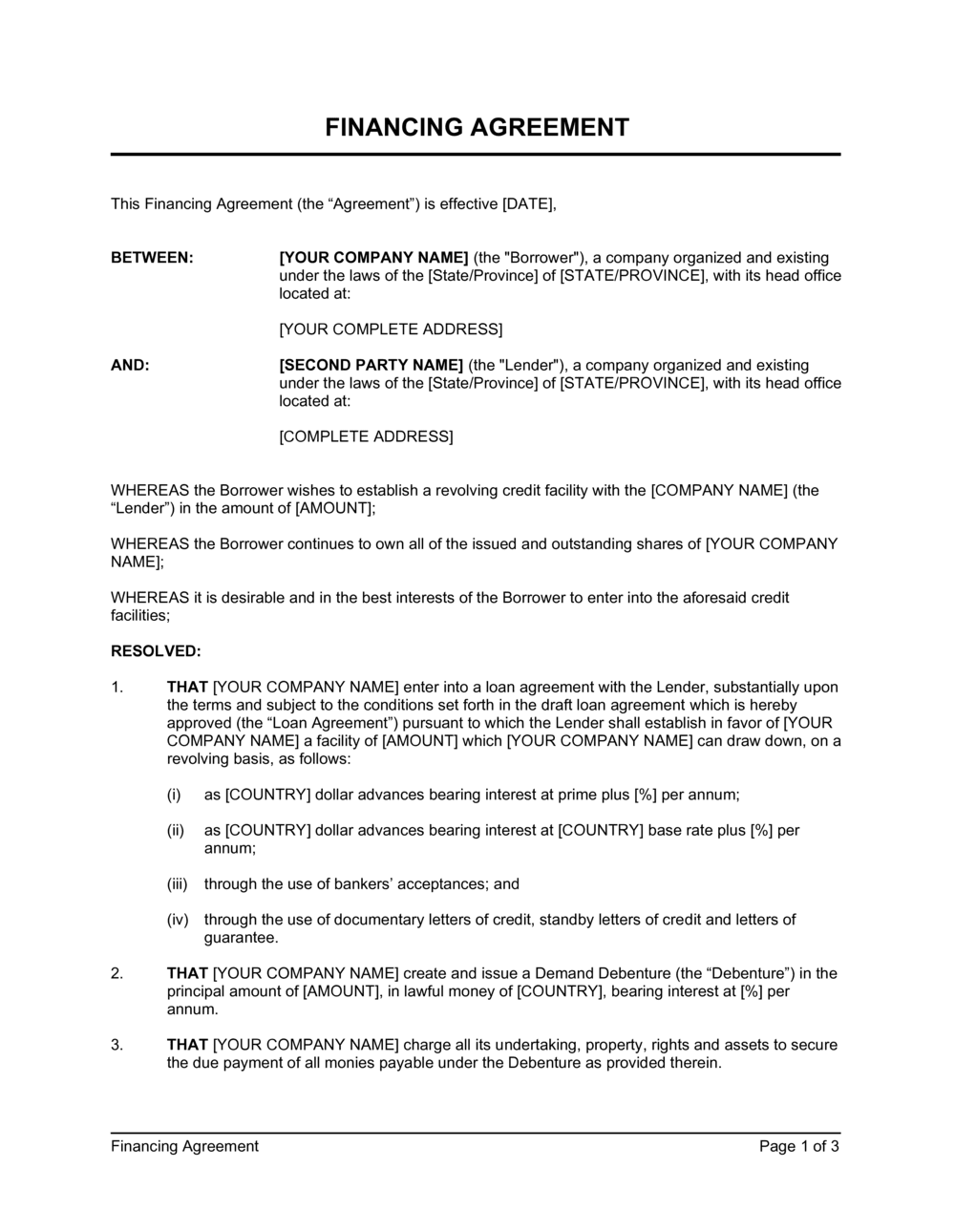

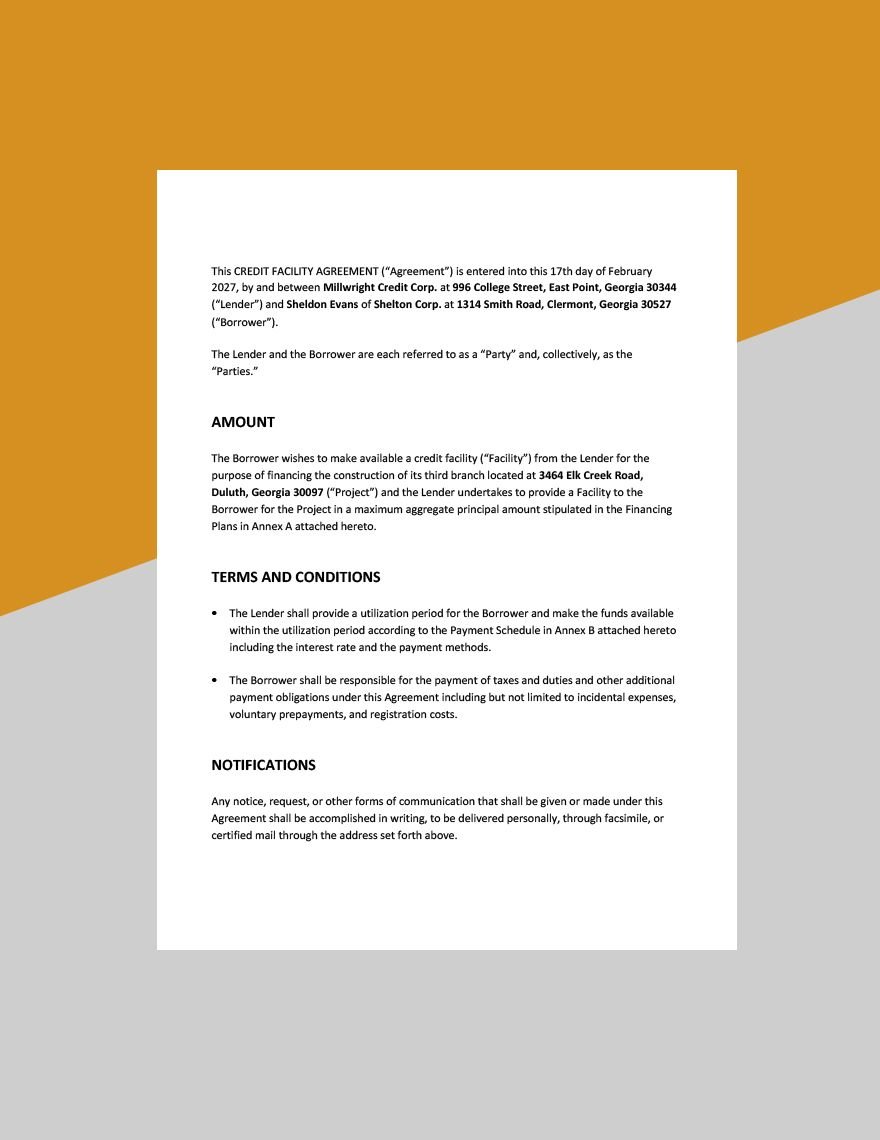

A Revolving Credit Facility Agreement is a type of loan that provides a business with access to funds for a specified period. Unlike a traditional loan, which typically has a fixed repayment schedule, a revolving credit facility allows businesses to draw down funds as needed, up to a pre-approved limit. This flexibility is incredibly valuable, particularly for businesses experiencing fluctuating cash flows or needing to manage short-term expenses. The agreement outlines the terms and conditions of the borrowing, including the interest rate, fees, and collateral requirements. It’s a contract that defines the relationship between the lender and the borrower, establishing clear expectations and responsibilities. A well-drafted agreement minimizes risk for both parties and fosters a stable and productive partnership.

Key Components of a Revolving Credit Facility Agreement

Let’s break down the essential elements typically included in a Revolving Credit Facility Agreement. These components are crucial for ensuring a smooth and legally sound transaction.

1. Parties Involved

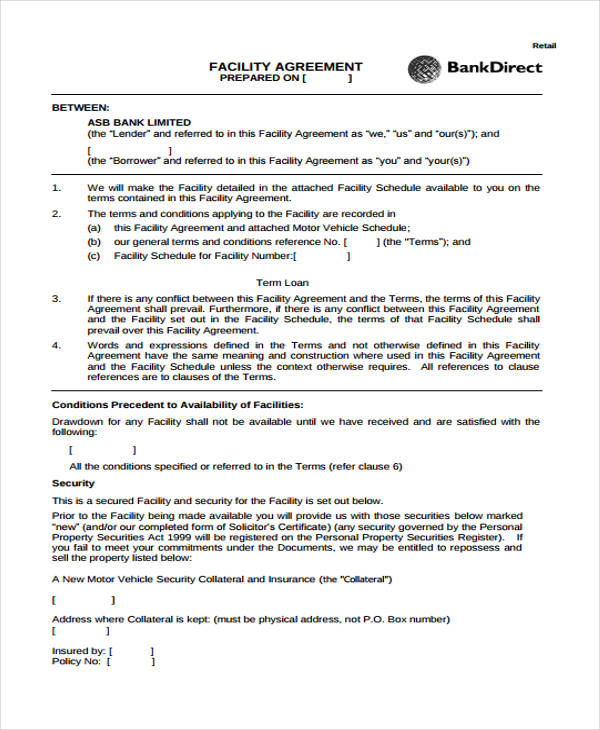

The agreement clearly identifies the parties involved – the borrower (the business seeking the financing) and the lender (the financial institution providing the funds). It’s vital to accurately represent the identities of all parties, including their legal addresses and contact information. A detailed description of the borrower’s business structure and its financial history is also included. Understanding the lender’s lending history and risk assessment process is equally important.

2. Facility Details

This section outlines the specific terms of the credit facility. Key details include:

- Loan Amount: The maximum amount of funds available to the borrower.

- Interest Rate: The annual percentage rate charged on the outstanding balance. This rate is often variable and tied to market indices.

- Fees: Any associated fees, such as origination fees, prepayment penalties, or late payment fees.

- Repayment Terms: The schedule for repayment, including the frequency of payments (e.g., monthly, quarterly) and the method of payment.

- Collateral: Assets pledged as security for the loan. The type and value of collateral are carefully defined.

3. Usage Restrictions

A significant aspect of the agreement is the restriction on how the funds can be used. The borrower must clearly define the specific purposes for which the funds are intended. This prevents misuse of the credit facility and protects the lender’s investment. Common uses include working capital, inventory purchases, marketing expenses, and equipment upgrades. It’s crucial to establish clear operational guidelines to ensure funds are used appropriately.

4. Default Provisions

This section outlines the consequences if the borrower fails to meet their obligations under the agreement. It typically includes provisions for acceleration of the loan, which means the lender can seize collateral to recover the outstanding debt. It also addresses potential legal remedies, such as lawsuits and arbitration. Understanding the default provisions is critical for mitigating potential losses.

5. Governing Law and Dispute Resolution

Specifying the governing law and the dispute resolution process is essential. This clarifies which jurisdiction’s laws will be applied to the agreement and how disputes will be resolved – through negotiation, mediation, arbitration, or litigation. A clear dispute resolution process minimizes the risk of costly and time-consuming legal battles.

The Importance of Legal Review

It is absolutely crucial that a Revolving Credit Facility Agreement be reviewed by legal counsel specializing in financial agreements. Errors or omissions in the agreement can have significant legal and financial consequences. A qualified attorney can ensure the agreement accurately reflects the parties’ intentions and complies with all applicable laws and regulations. They can also advise on the best way to structure the agreement to minimize risk and maximize the benefits for both the borrower and the lender.

Beyond the Basics: Additional Considerations

While the core elements outlined above are essential, several additional considerations should be taken into account when drafting or reviewing a Revolving Credit Facility Agreement.

1. Financial Projections

A detailed financial projection demonstrating the business’s ability to repay the loan is vital. This includes projected revenue, expenses, and cash flow. The lender will scrutinize these projections to assess the borrower’s creditworthiness.

2. Business Plan

A comprehensive business plan outlining the company’s strategy, market analysis, and competitive landscape strengthens the borrower’s case for the loan.

3. Credit History and Financial Statements

Reviewing the borrower’s credit history and financial statements provides insights into their financial stability and ability to manage debt.

4. Security Considerations

The type and value of collateral offered to secure the loan significantly impacts the lender’s risk assessment. A robust security plan is essential.

The Future of Revolving Credit Facilities

Revolving credit facilities are increasingly popular, driven by the need for businesses to adapt to changing market conditions and manage fluctuating cash flows. Technology is playing a growing role in streamlining the process of creating and managing these agreements. Digital platforms are facilitating faster and more efficient document sharing and contract execution. As technology continues to advance, we can expect to see even more innovative approaches to managing revolving credit facilities in the future.

Conclusion

The Revolving Credit Facility Agreement Template is a powerful tool for businesses seeking to access capital. By carefully considering the key components and seeking expert legal guidance, businesses can navigate this complex financial arrangement with confidence and maximize the benefits of this valuable financing option. A well-structured agreement, coupled with a solid business plan and accurate financial projections, significantly increases the likelihood of a successful and mutually beneficial relationship with a lender. Ultimately, a robust and legally sound agreement is the foundation for a thriving business.

Conclusion

The Revolving Credit Facility Agreement Template represents a critical tool for businesses seeking to secure funding and manage their financial operations. Understanding the intricacies of this agreement, coupled with diligent legal review, is paramount for both borrowers and lenders. By prioritizing clear communication, robust security, and a proactive approach to risk management, businesses can leverage the power of revolving credit facilities to achieve their strategic goals and foster sustainable growth. The continued evolution of technology and regulatory frameworks will undoubtedly shape the future of these agreements, requiring ongoing adaptation and refinement.