The process of recovering funds from a credit dispute can be incredibly frustrating and complex. A well-crafted credit dispute letter is crucial for effectively communicating your concerns and increasing your chances of a favorable resolution. This guide provides a comprehensive overview of what to include in a credit dispute letter, ensuring you present your case clearly and professionally. Understanding the nuances of this process is vital for anyone facing a financial setback. Credit Dispute Letter Template – a standardized format helps ensure your message is easily understood and readily accepted. This template is designed to be adaptable to various situations, but remember to tailor it specifically to your circumstances.

Why is a Credit Dispute Letter Important?

Credit disputes often arise when you believe you’ve been wrongly denied credit, charged incorrectly, or experienced a service failure. A formal letter provides a documented record of your concerns, demonstrating your efforts to resolve the issue. It’s a powerful tool for asserting your rights and potentially securing a refund or compensation. Without a clear and well-written letter, it can be difficult to convince the creditor to reconsider their position. Furthermore, it’s a valuable document for future reference and potential legal action. The process can be lengthy and require careful attention to detail, making a professional letter a key component of a successful outcome.

Understanding the Basics of Credit Dispute Letters

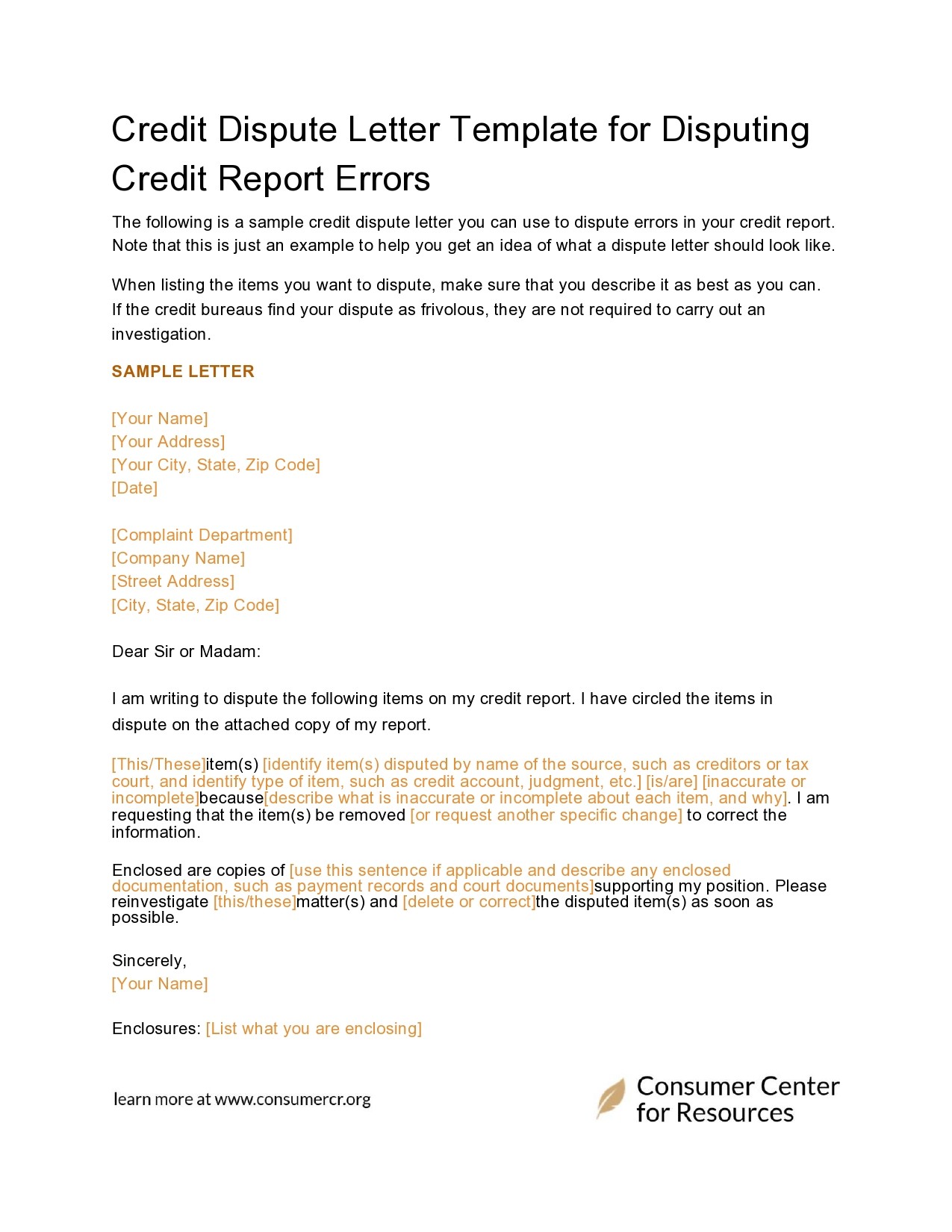

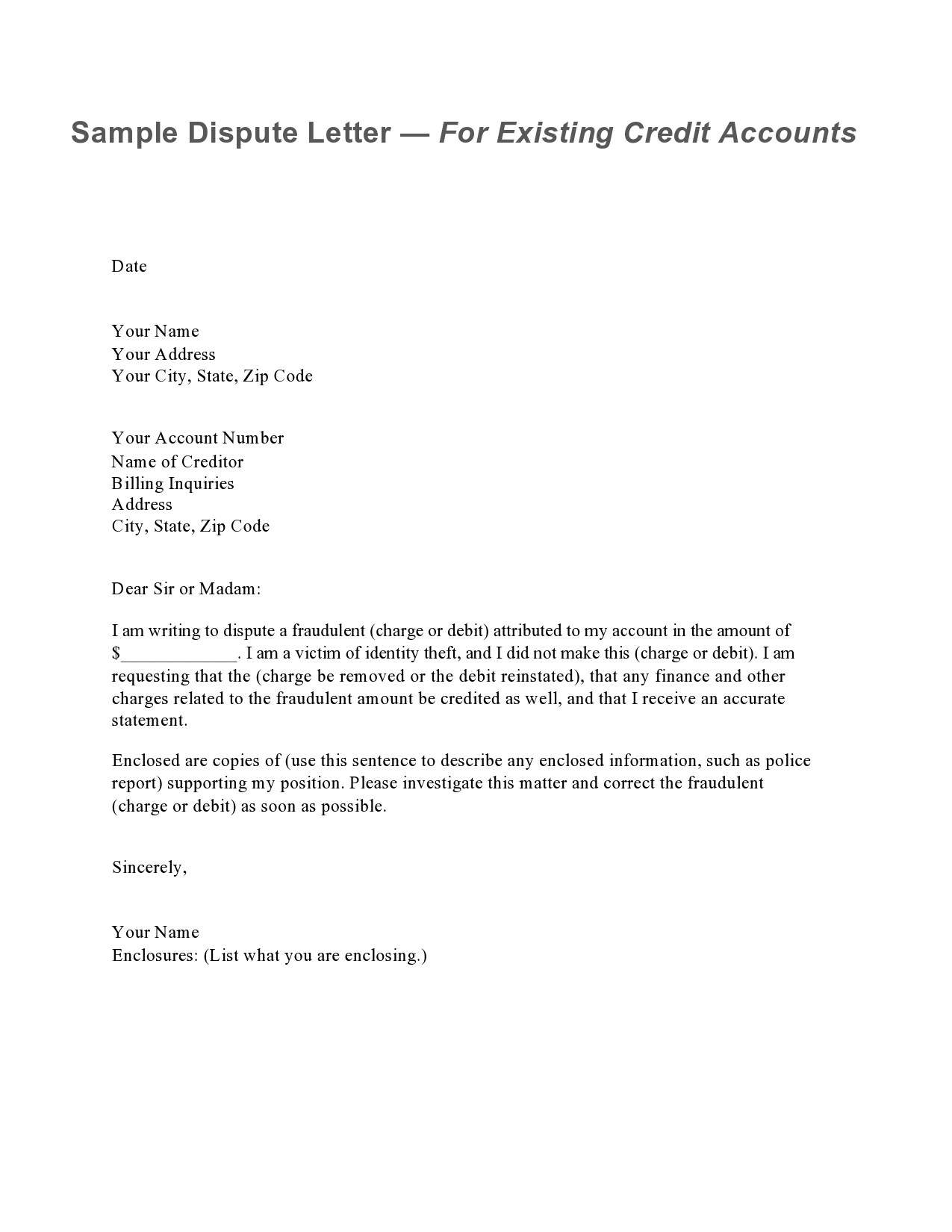

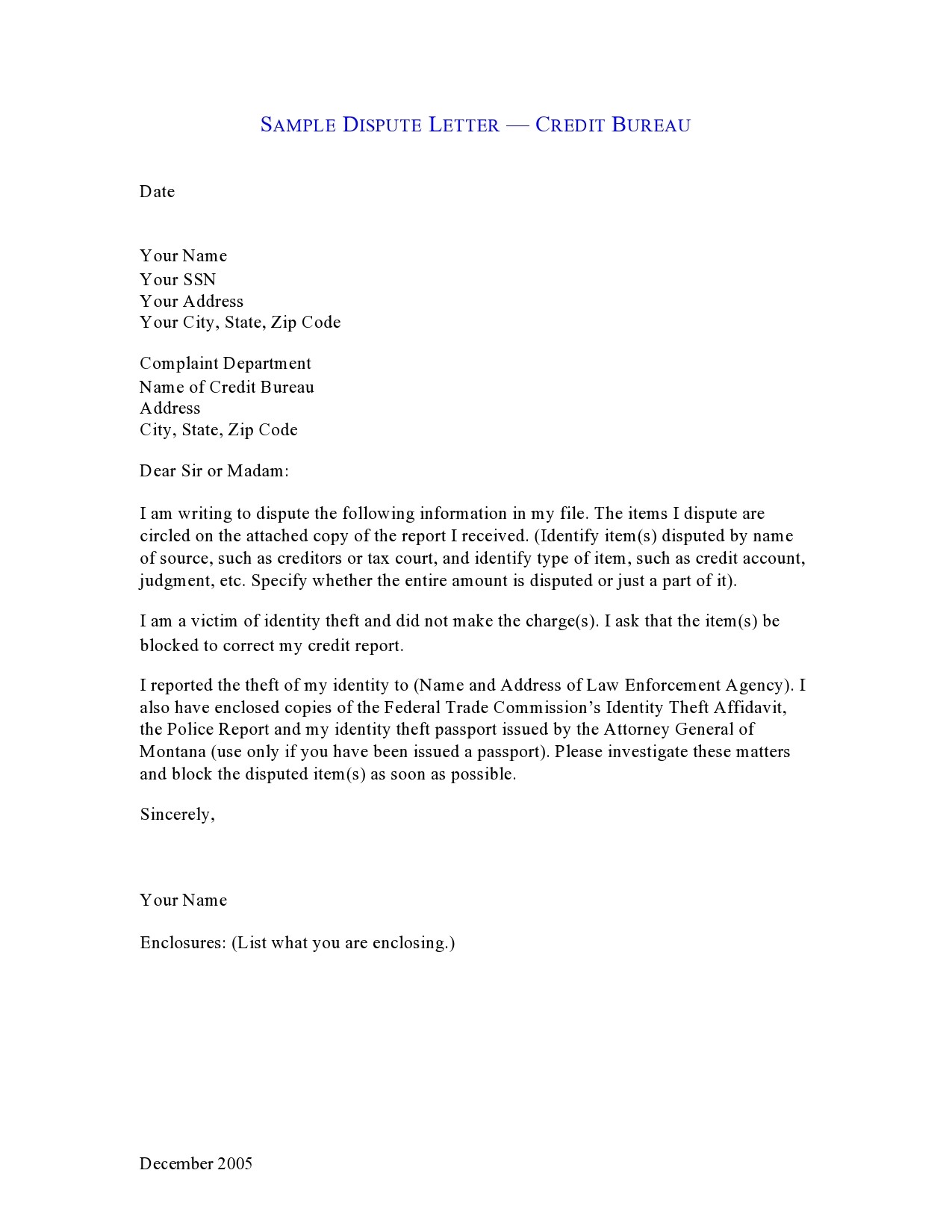

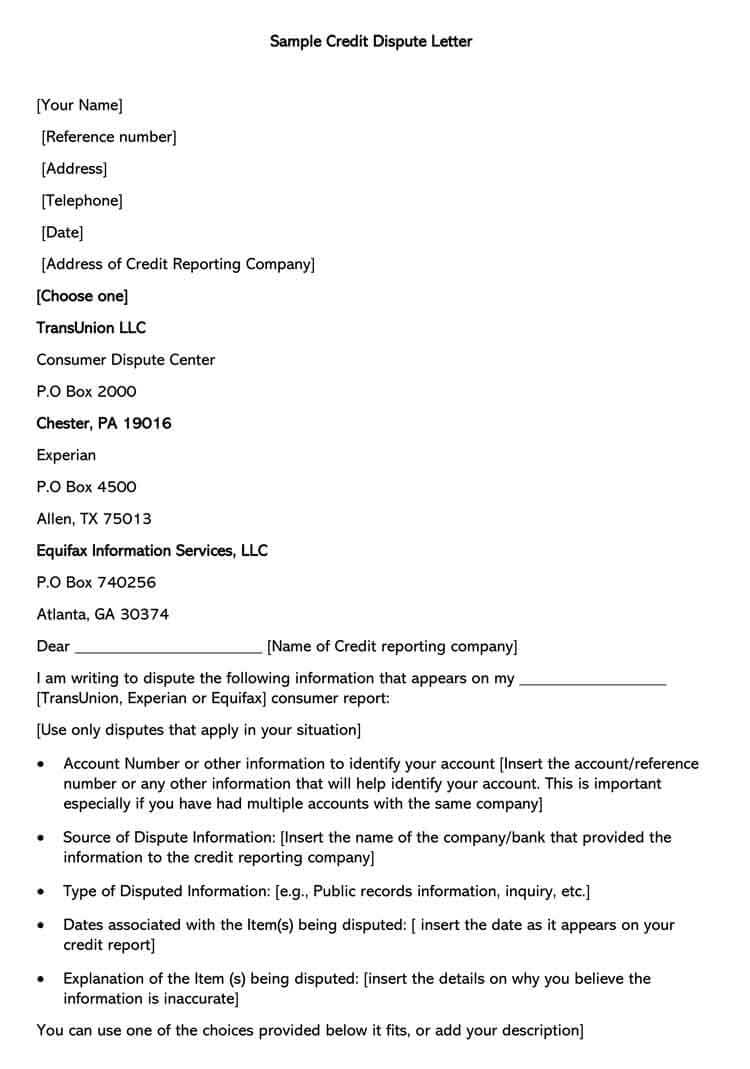

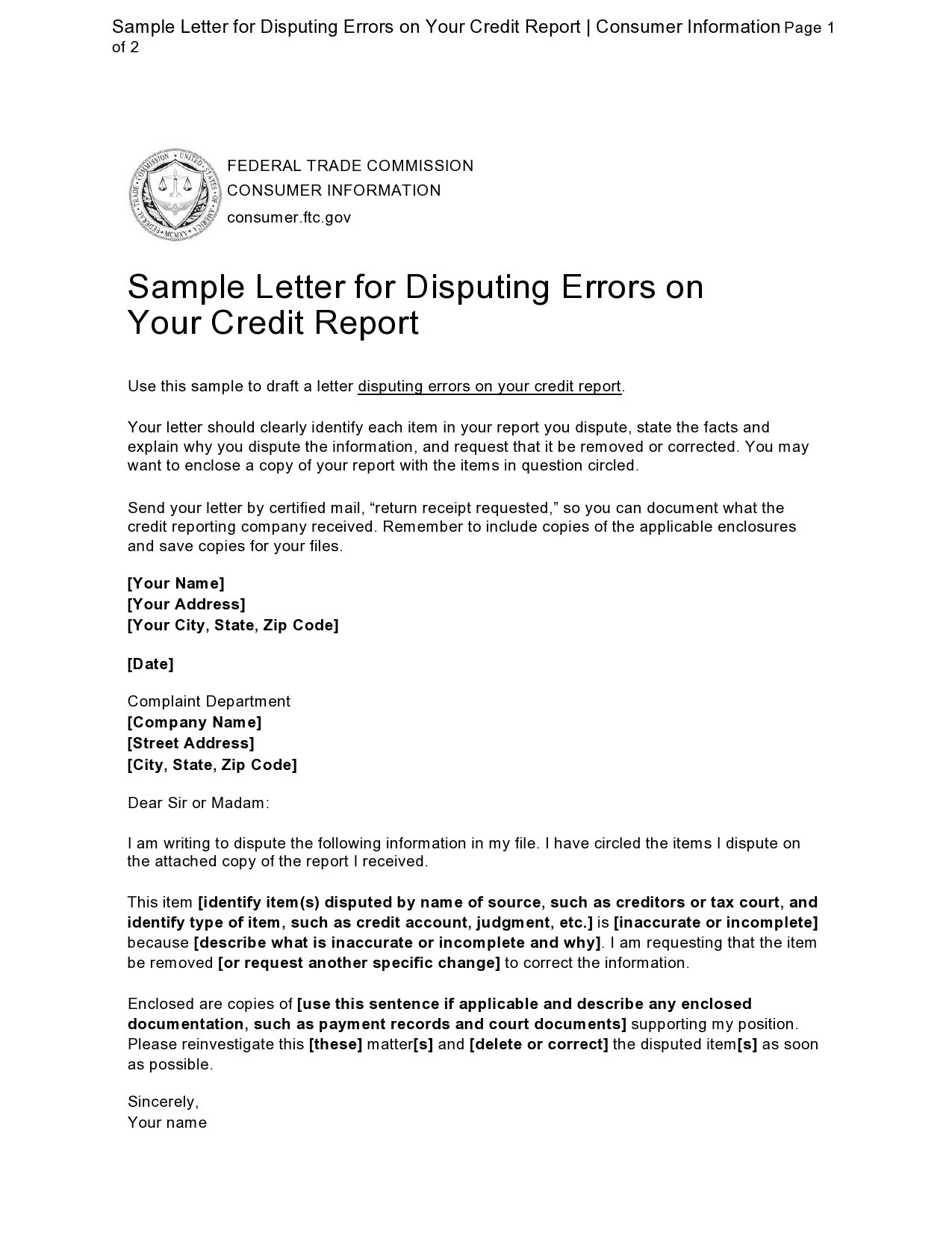

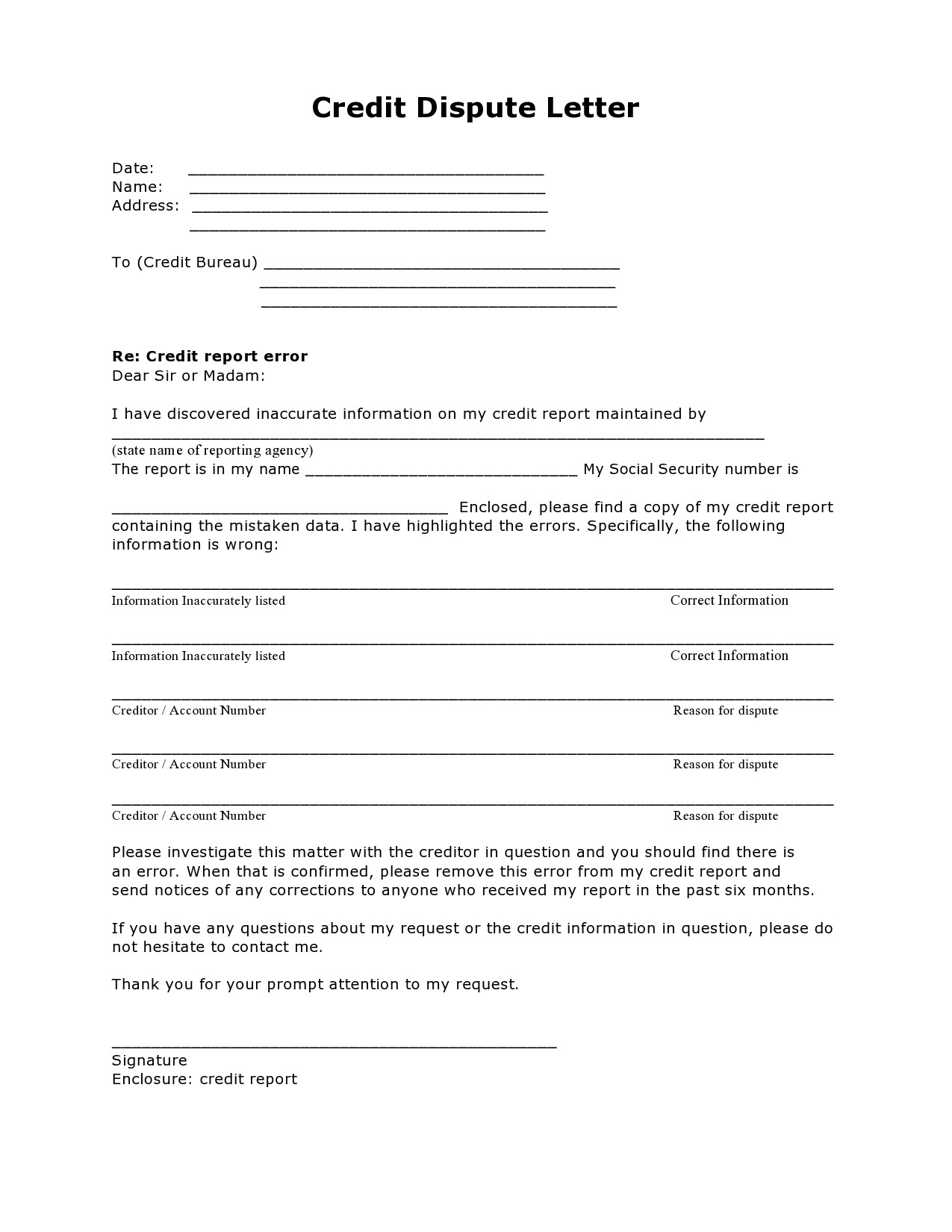

A credit dispute letter is a formal written communication between you and the creditor, outlining the circumstances surrounding the dispute and requesting a specific resolution. It’s not just a casual email; it’s a structured document designed to be persuasive and legally sound. The goal is to clearly articulate the problem, provide supporting evidence, and state your desired outcome. The template provides a framework, but you’ll need to personalize it with specific details relevant to your situation. It’s important to keep a copy of the letter and any supporting documentation for your records.

The Essential Components of a Credit Dispute Letter

Let’s break down the key sections of a credit dispute letter. Each section should be clearly articulated and supported by evidence.

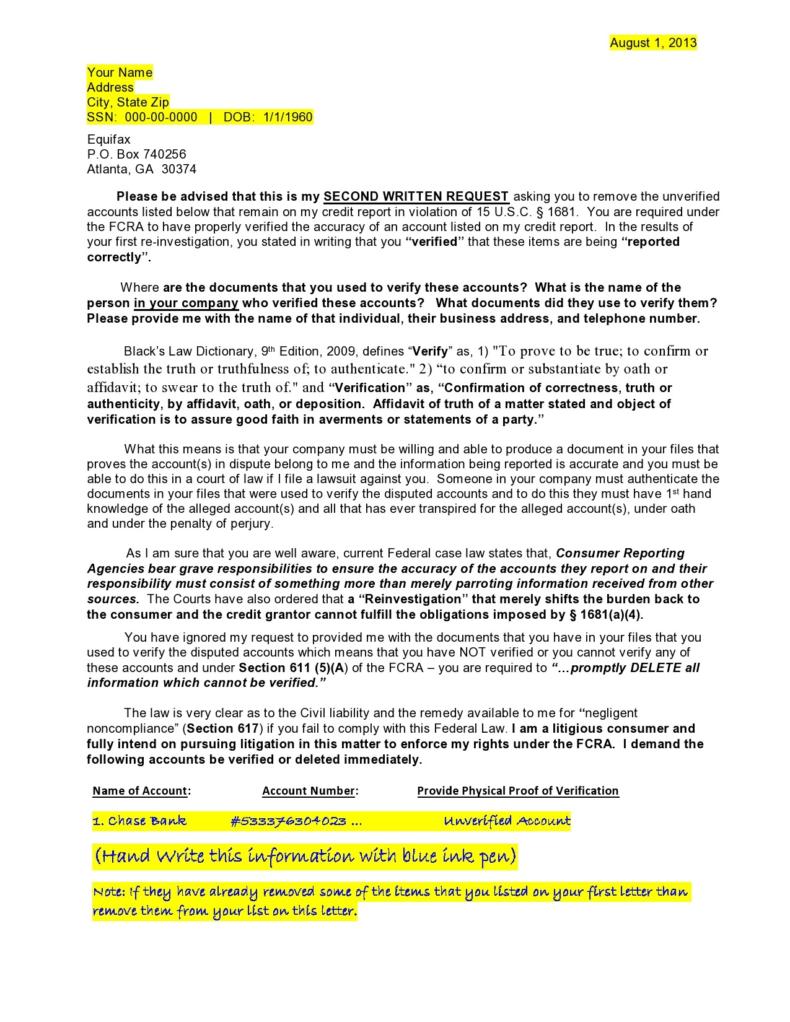

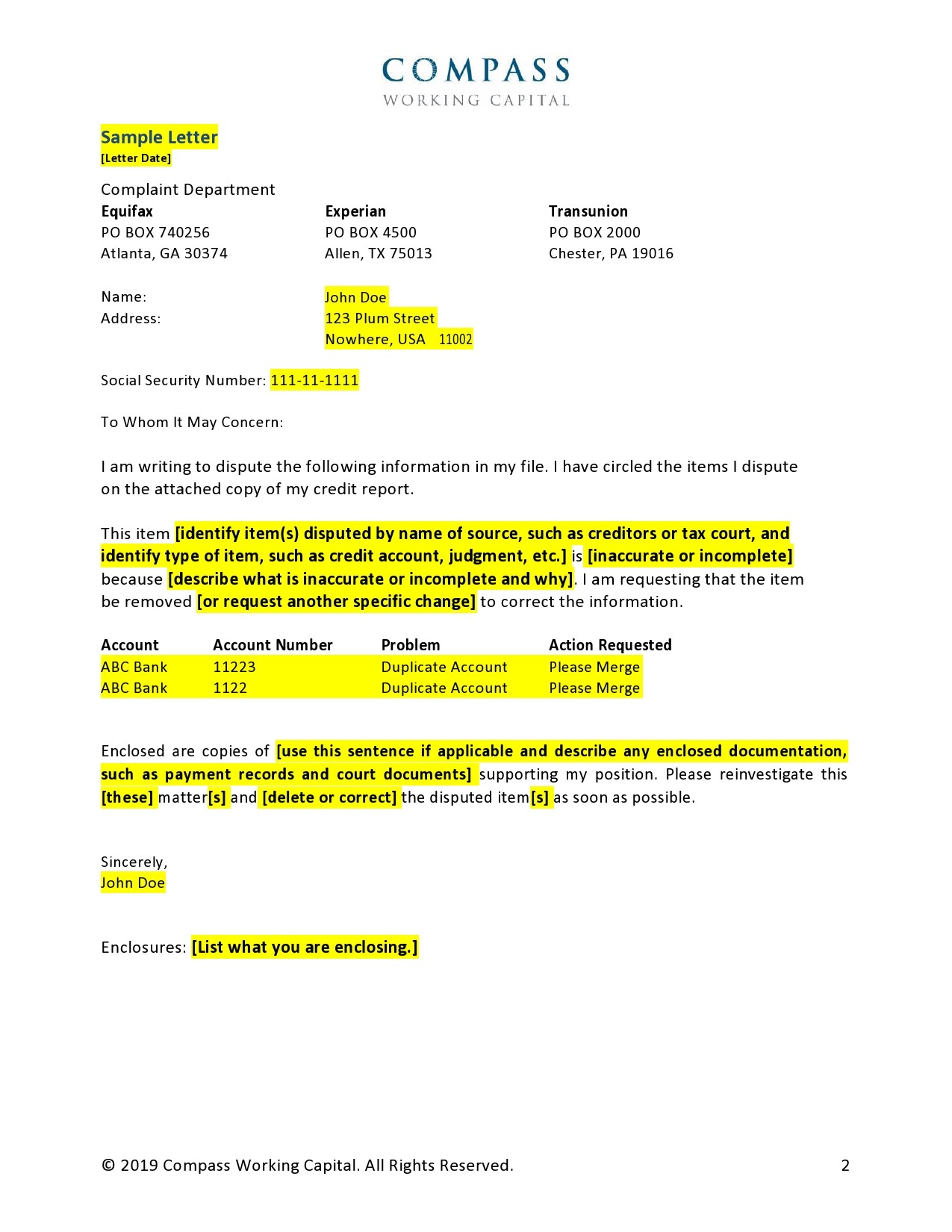

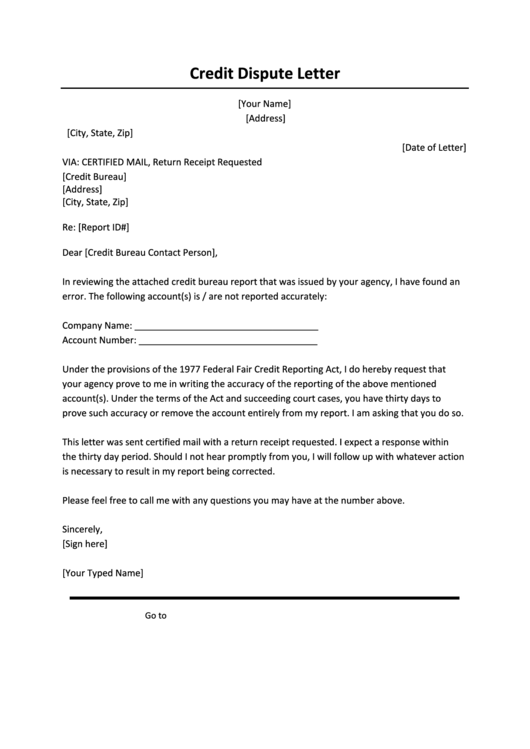

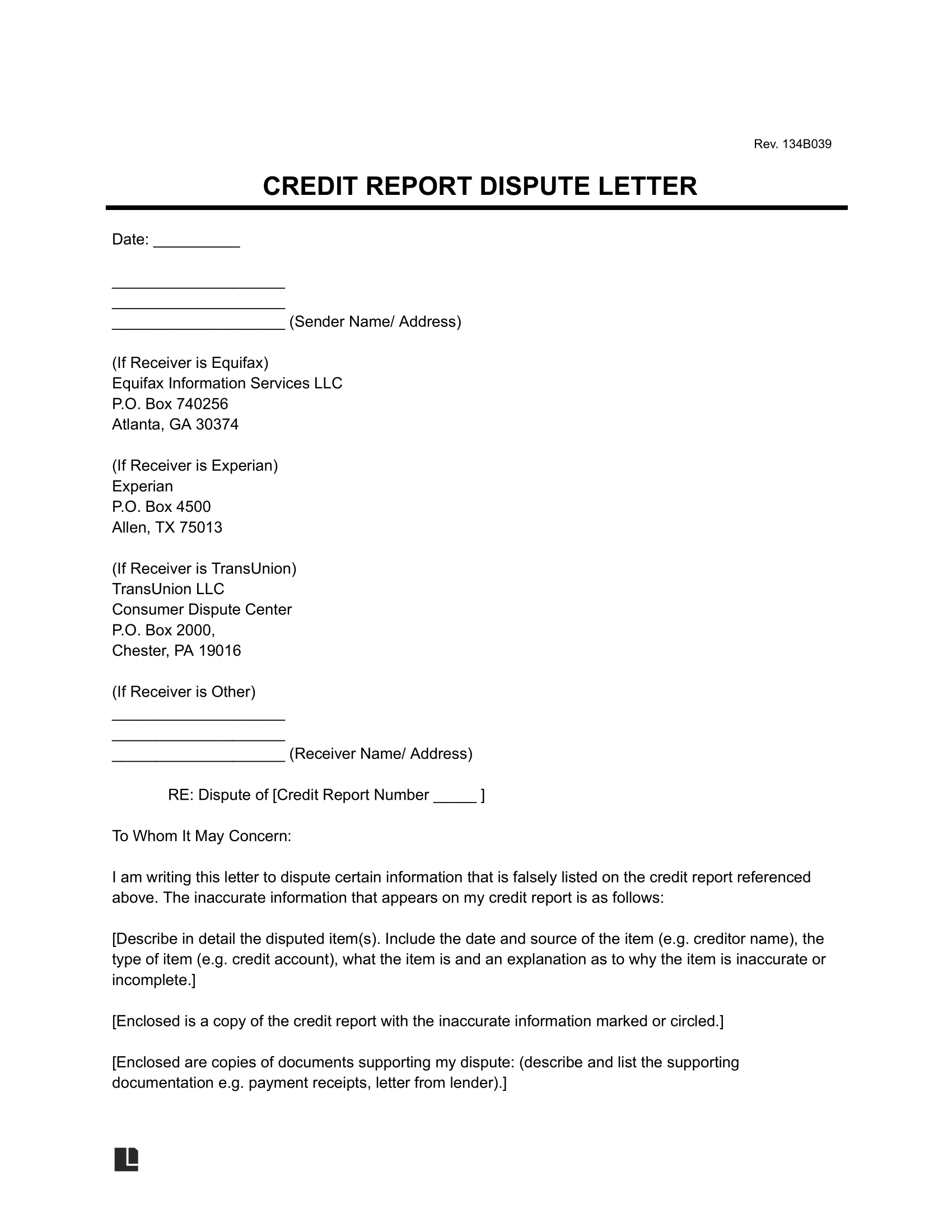

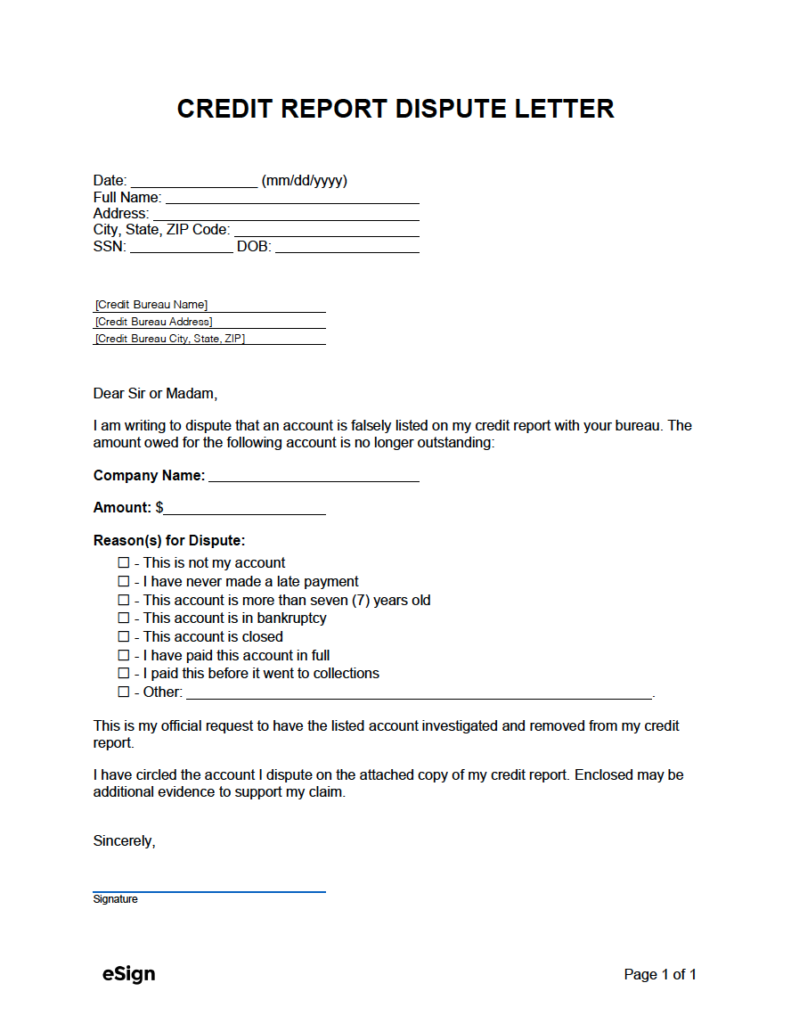

Section 1: Header and Contact Information

Begin your letter with a clear and professional header. Include your full name, address, phone number, and email address. This information is essential for the creditor to contact you and locate your account. It’s good practice to include a date of service or transaction.

Section 2: Introduction – Clearly State the Dispute

Immediately state the purpose of your letter – to dispute a credit charge or claim. Begin with a concise statement of the issue. For example: “I am writing to dispute a charge of [Amount] for [Description of Service/Product] which I believe was incorrectly applied to my account.” This sets the tone and immediately conveys the core of your concern.

Section 3: Detailed Account Information

Provide a brief overview of your account details. This includes the creditor’s name, account number, and the date of the transaction. This information is crucial for the creditor to quickly locate your account. Include the date of the transaction, the amount charged, and a brief description of the service or product involved.

Section 4: Explanation of the Dispute – Provide Your Case

This is the most important section. Clearly and concisely explain why you believe the charge is incorrect. Provide specific details and supporting evidence. This is where you’ll elaborate on the circumstances that led to the dispute. Consider including:

- The Original Transaction: Provide a copy of the original invoice or receipt.

- The Service/Product Description: Clearly describe the service or product you received.

- The Date of Service: Record the exact date of the transaction.

- Any Relevant Correspondence: Include copies of any emails, letters, or other communications you’ve had with the creditor regarding the issue.

- Evidence of Errors: If you believe there was an error, provide evidence to support your claim. This could include screenshots, photos, or other documentation.

Example Explanation: “On [Date], I received a bill for [Amount] for [Description of Service]. However, I have since discovered that [Explain the error – e.g., the service was not rendered as described, the price was incorrect, etc.]. I have attached a copy of the original invoice and a screenshot of the online service agreement.”

Section 5: Requested Resolution – State Your Desired Outcome

Clearly state what you are requesting as a resolution. Be specific and reasonable. Options include:

- Refund: Request a full or partial refund.

- Credit: Request a credit towards a future bill.

- Reversal of Charge: Request the charge to be reversed.

- Explanation of the Charge: Request a detailed explanation of the charge.

For example: “I request a full refund of [Amount] to be credited back to my account. I also request a detailed explanation of the charges on this bill.”

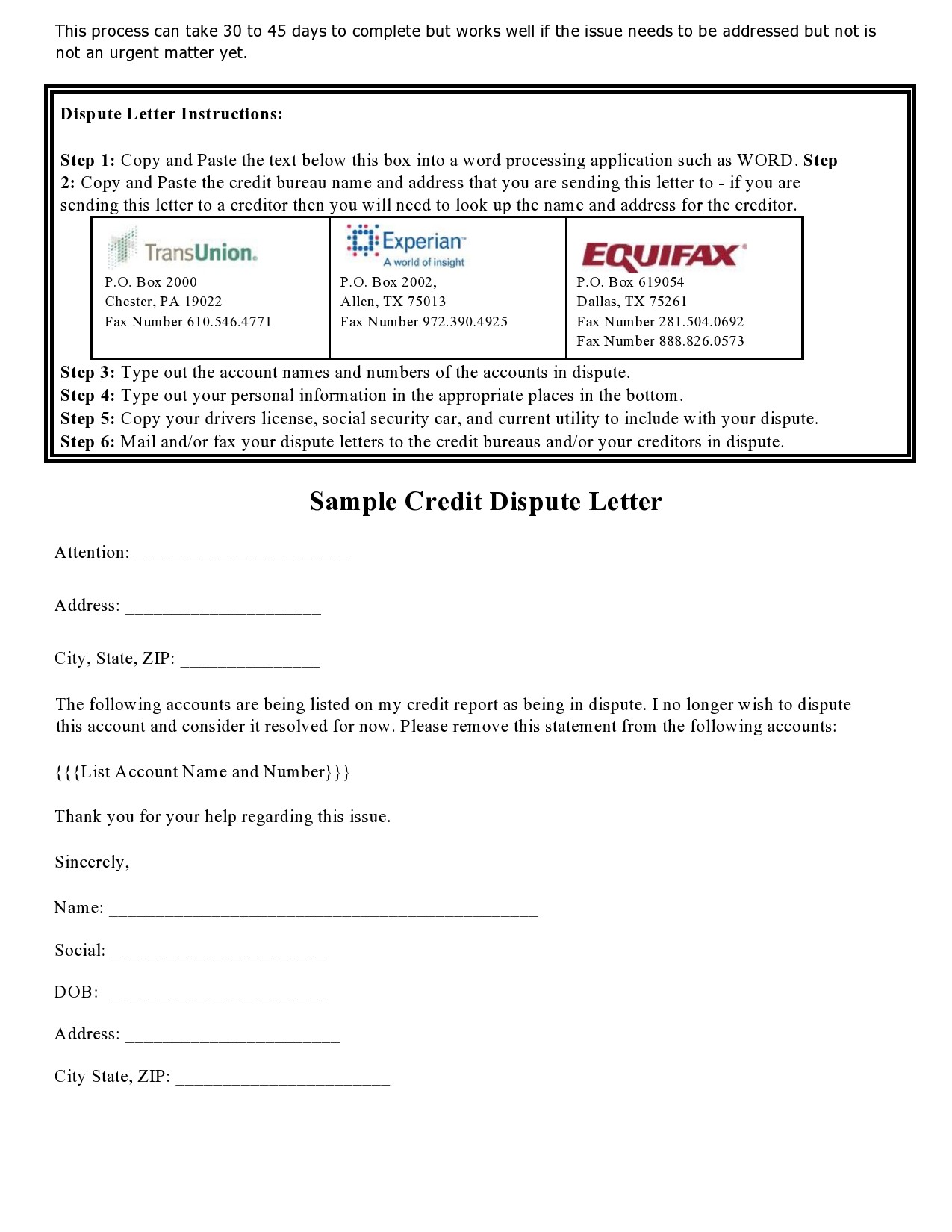

Section 6: Supporting Documentation – Attach Relevant Files

Attach copies of all supporting documentation, such as invoices, receipts, contracts, emails, and any other relevant materials. Make sure to clearly label each attachment. Organize your documents logically.

Section 7: Closing and Signature

End your letter with a polite and professional closing. Sign your name and include your contact information again. Thank the creditor for their time and consideration.

Section 8: Certified Copy (Optional but Recommended)

Consider sending your letter via certified mail with return receipt requested. This provides proof that the creditor received your letter.

Important Considerations for a Strong Credit Dispute Letter

- Be Polite and Professional: Maintain a respectful tone throughout the letter, even if you are frustrated. Anger can undermine your credibility.

- Be Clear and Concise: Avoid jargon and use straightforward language. Get straight to the point.

- Be Organized: Present your information in a logical and easy-to-follow manner.

- Keep a Copy: Always keep a copy of the letter and all supporting documentation for your records.

- Follow Up: If you don’t receive a response within a reasonable timeframe (typically 30-60 days), follow up with a phone call or email.

Conclusion

Navigating the credit dispute process can be challenging, but a well-crafted credit dispute letter is a powerful tool for protecting your rights. By following the guidelines outlined in this guide, you can increase your chances of a successful resolution and minimize the potential for further financial hardship. Remember to tailor the letter to your specific situation and always maintain a professional and respectful tone. The consistent use of the Credit Dispute Letter Template will significantly improve your ability to effectively advocate for yourself. Proper documentation and a clear, reasoned argument are key to a favorable outcome.

Conclusion

The credit dispute letter serves as a critical communication tool, enabling individuals to effectively address and resolve financial discrepancies. By meticulously adhering to the outlined structure and incorporating the essential components, one can significantly enhance the likelihood of a successful resolution. Ultimately, a thoughtfully drafted letter demonstrates a proactive and determined approach to protecting one’s financial interests. The consistent application of the Credit Dispute Letter Template will undoubtedly contribute to a more streamlined and satisfactory dispute resolution process.